Democrats throw in the towel, admit Obamacare is not affordable

According to a Senate presentation by Sen. Ron Johnson of Wisconsin, new data shows Alaska has experienced one of the smallest increases in employer-sponsored health insurance premiums in the nation since Obamacare took effect, yet one of the largest spikes in Obamacare marketplace premiums.

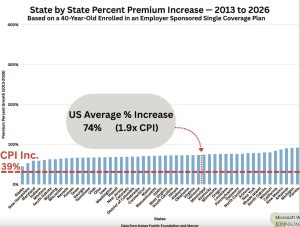

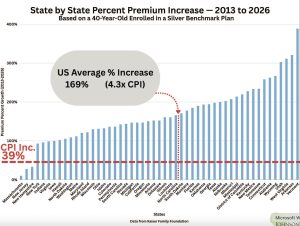

Two charts presented by Johnson, based on Kaiser Family Foundation and Mercer data, tell the story: Private health care costs are not exploding, but Obamacare premiums are soaking the families and small businesses of the state.

From 2013 to 2026, the average employer-sponsored single-coverage plan for a 40-year-old in Alaska has risen by roughly 45%, which is a rate slightly higher than overall inflation during the same period, 39%. The national average increase for employer plans is 74%, or nearly double the rate of inflation.

But when it comes to Obamacare “Silver” plans, which form the backbone of the Affordable Care Act’s individual marketplace, Alaska’s premiums have exploded. The data show roughly a 200% increase, well above the national average of 169%, and more than four times the Consumer Price Index.

The contrast is striking.

While Alaska’s employer-based plans have remained relatively stable, suggesting a competitive private insurance market, the state’s Obamacare premiums have soared far faster than the rest of the country.

That means the same Alaskan who gets coverage through a job has close to inflation-level increases, but if that person buys coverage through the federal marketplace, they’re being hit with some of the highest costs in America. Typically, this means small business owners, their employees, and sole proprietors are getting hosed by Obamacare.

In fact, Alaska is getting raked relative to what the actual competitive marketplace reflected by employer-sponsored plans is showing.

This is a fact that the Senate Democrats have admitted: They repeatedly took to the floor of the Senate over the last month to state how unaffordable their insurance plan has become.

When the Affordable Care Act was enacted in 2010, its architects, and President Barack Obama, promised it would drive down costs through competition and regulation. But for Alaska, the opposite has happened.

SUPERCUT!

Turns out everything @BarackObama said to sell ObamaCare was one big fat lie after another pic.twitter.com/tYoApJELAK

— Tom Elliott (@tomselliott) October 31, 2025

Due to its small population, limited risk pool, and high health care delivery costs, Alaska’s marketplace became one of the most expensive in the nation almost immediately after the ACA went into effect. By 2017, Alaska’s individual market premiums were more than double the national average. A state-level reinsurance program helped stabilize the market somewhat, but prices have never returned to pre-ACA levels, and the stabilization comes at a cost to other state services.

Here is the breakdown of the states with the highest increases for Obamacare consumers:

- Wyoming: Highest Obamacare increase, but among the lowest employer-sponsored increases (difference of ~44 rank positions).

- Utah: Very high Obamacare increase, low employer-sponsored increase (difference of ~34 rank positions).

- Alaska: High Obamacare increase, lowest employer-sponsored increase (difference of ~33 rank positions).

- Tennessee: High Obamacare increase, low employer-sponsored increase (difference of ~31 rank positions).

- West Virginia: Very high Obamacare increase, relatively low employer-sponsored increase (difference of ~27 rank positions).

These states stand out because their Obamacare premiums far outpaced the increases in market-based health insurance.

In fact, Obamacare premium increases significantly outpace their employer-sponsored increases, often by 200-350 percentage points based on visual estimates from the charts’ scales.

Now, Johnson’s analysis suggests that, even adjusted for inflation, Obamacare premiums in Alaska have grown roughly five times faster than general consumer prices, while the employer-based plans that existed long before the ACA have barely outpaced inflation at all.

The data shows what many Alaskans already feel in their wallets: the federalized health care system simply doesn’t work for Alaska, where a high number of people are on government-employment or Indian Health Service healthcare plans.

If Obamacare was meant to expand affordability, its marketplace in Alaska has done the opposite, creating a two-tiered system where those with employer coverage are protected, and those forced into the Obamacare “marketplace” to buy their own insurance face the steepest costs in America.

8 thoughts on “Alaska pays the price: Obamacare premiums skyrocket while employer plans stay flat”

Because the Dems have such a warm place in their hearts for Alaskans, unless they’re Natives that remain” on the reservation”

A good guess is giving government money to an Insurance company is not a good idea

One third of Alaskans are on medicaid. Average state participation is around 21 percent. 27000 Alaskans have a plan through the ACA. From 2013 to 2022 the uninsured rate dropped by 7.5 per cent. Maybe the fact that hospitals are actually being paid for their services is keeping the cost down for others. Which is the whole idea of the ACA

Hogwash.

Providence charges nearly 4x the national average for their services.

Why?

Because they can -they have almost 0 competition!

10+ years ago their CEO admitted as much in an interview in the ADN and nobody made a peep. It’s still happening, folks.

In Alaska —- Employer based plans stayed flat …… well who is the biggest employer in Alaska? Government. Particularly the state.

I think Bernie Sanders said it best when he admitted that the current system (Obamacare) is “wildly inefficient bureaucratic system” and “It is unaffordable” the part he gets wrong is wanting to continue to subsidize that wildly inefficient and unaffordable system.

Let’s be honest medical costs have skyrocketed. Obama Care has nothing to do with senior assisted living. Check out the monthly rates at Baxter or Aspen. We are living longer and new expensive medications mean much higher costs as we age.

Time will always ‘out’ the truth.